The IP Base Pricing Model (IBPM)

A Framework for Pricing Novel Technology Before Market Entry

You’ve built something new. A custom semiconductor design. A novel algorithm. A piece of deep-tech IP that took years, millions of dollars, and a team to create.

Now you need to price it.

The problem: there are no comparable deals to benchmark against. IP licensing data is highly confidential. What’s publicly available is either too aggregated to be useful or doesn’t cover your specific situation. Customer dependency, available alternatives, seller urgency, value chain economics—all of these affect price, and none of them show up in databases.

So most founders do what they have to: make an educated guess. Add a markup. Hope it sticks.

I ran into this problem pricing novel IP at Anthriq. Rather than guessing, I built a framework to break down the assumptions into granular, testable pieces. This is the explainer for that framework.

The Real Problem: Lack of Reference Data

Traditional IP valuation methods exist, but they don’t solve the pre-market pricing problem.

Income approach: Requires revenue projections that don’t exist for novel tech.

Market approach: Requires comparable transactions. But licensing deals are confidential. Customer dependency varies. Strategic importance varies. Available alternatives vary. The data you’d need to do this properly isn’t published anywhere.

Cost approach: At least grounded in reality—you know what you spent. But it doesn’t account for customers over time, IP characteristics, or commercial longevity.

The gap: you need a price to enter negotiations, but you have no objective reference point to anchor it.

What IBPM Does

The IP Base Pricing Model (IBPM) calculates a base price by forcing you to decompose your assumptions into specific, quantifiable inputs:

What did development actually cost?

What return do you need to justify the risk?

How many customers will you have, and when?

What kind of IP is this—commodity or moat?

How long will this IP remain commercially relevant?

Each assumption is explicit. Each one can be stress-tested. The output is a base price grounded in your specific situation, not a generic industry multiple.

The formula,

Where:

C_dev: Total development cost

r_req: Required annual return

T_fixed: Payback period (fixed period to cover your cost)

F_NPV: Net present value of customer stream over IP lifetime

CAF: Cost Affecting Factor (weighted score of IP characteristics)

LF: Lifetime Factor (asymptotic adjustment for commercial longevity)

What it means

Development Cost × Required Return

The numerator represents what you need to recover.

Development cost includes everything: R&D salaries, prototyping, equipment, IP filing, regulatory testing, failed experiments. Everything you spent to create the IP.

Required return reflects the risk. Early-stage deeptech has technology risk, market risk, execution risk. Your investors have alternatives. 30-60% annual returns are standard for this risk profile. Use whatever rate reflects your actual situation.

If you spent $4.2M and need 40% returns over 3 years: $4.2M × (1.4)³ = $11.5M.

NPV Factor: Present Value of Customer Stream

The NPV Factor represents the effective size of your customer base in present value terms.

Not just how many customers you expect—but when you’ll get them, adjusted for time value of money and churn.

A customer in Year 1 contributes more to cost recovery than a customer in Year 6, because of discounting. The NPV Factor accounts for this properly. For each year, take projected customers × growth factor, then discount back to present value—sum across all years to get the effective customer base in today's terms.

Higher NPV_factor = More customer revenue capacity = Lower base price needed

Lower NPV_factor = Less customer revenue capacity = Higher base price needed

Example: Starting with 2 customers, growing 85%/year, 8% churn, over 8 years, with a 15% discount rate → NPV Factor of ~48.3.

Cost Affecting Factor (CAF): IP Characteristics

Not all IP should be priced identically, even with the same development cost.

CAF is a weighted scoring matrix that adjusts pricing based on your IP’s characteristics. You can add or remove characteristics according to your judgement.

Price-increasing/decreasing factors:

Technical complexity - How complex you think is development

Moat strength - Can it be replaced easily today ?

Regulatory barriers - Does it need to cross some regulatory check

Standalone importance - Can you commercialize your IP without any dependency

Integration complexity

Patents granted / coverage

Expected market demand

You score each factor 0-10, weight by importance, and get a CAF score typically between 3 and 9.

A generic software module might score lower. A patented hardware IP with regulatory approval might score higher. CAF ensures the math reflects the IP’s actual characteristics, not just what it cost to build.

Lifetime Factor (LF): Commercial Longevity

This is where I got a little creative and made things complex because my formula was performing bananas over simulated time. Longer IP lifetimes enable cost spreading across more years. But pricing power decays as technology matures.

The Lifetime Factor uses an asymptotic curve: early years of IP life add significant pricing benefit, later years add progressively less.

This reflects economic reality. Doubling IP lifetime from 7 to 14 years doesn’t halve the required price—because the second 7 years contribute less as competition increases and the tech commoditizes.

Worked Example:

Custom DSP Module for Automotive ADAS

Scenario: You’ve built a custom digital signal processing module for automotive Advanced Driver Assistance Systems (ADAS). It handles sensor fusion for Level 2+ autonomous features.

Inputs:

Development cost: $2.8M

Required return: 45%, over 3 years

Customer projection: Start with 3 Tier-1 suppliers, grow 60%/year, 5% churn, 10-year IP lifetime

Discount rate: 12%

CAF score: 5.2 (moderate technical complexity, competitive market but strong integration dependencies)

Calculation:

Numerator: $2.8M × (1.45)³ = $8.54M

NPV Factor: 62.7 (calculated across 10-year customer stream with growth/churn/discounting)

Lifetime Factor: 2.34 (10-year lifetime with asymptotic decay)

Denominator: 62.7 × 5.2 × 2.34 = 763

IBPM Base Price: $8.54M / 763 = $11,200 per license

This is the base. Actual market prices for automotive semiconductor IP typically run 5x to 20x the base, depending on the OEM’s volume commitments and exclusivity terms. Mind you, this is the fixed fee, IP deals usually are more complex; adding royalties, market premiums, integration cost, AMCs etc.

For context: if a Tier-1 supplier integrates this into modules going into 500K vehicles/year, that’s $0.11–$0.27 per vehicle—economically viable for both parties.

What This Framework Is Not

IBPM is not a guaranteed market price predictor. It’s a tool to ground your assumptions in logic.

The output depends entirely on the inputs. If you’re overly optimistic about customer projections, you’ll underprice. If you overestimate your moat (CAF), you’ll overprice. The framework doesn’t protect you from bad assumptions—it just makes them explicit and testable.

It won’t match every real-world deal. Strategic partnerships, fire sales, network effects, customer bargaining power—all of these create variance around the base price. Some deals will close at 0.5x base, others at 10x base.

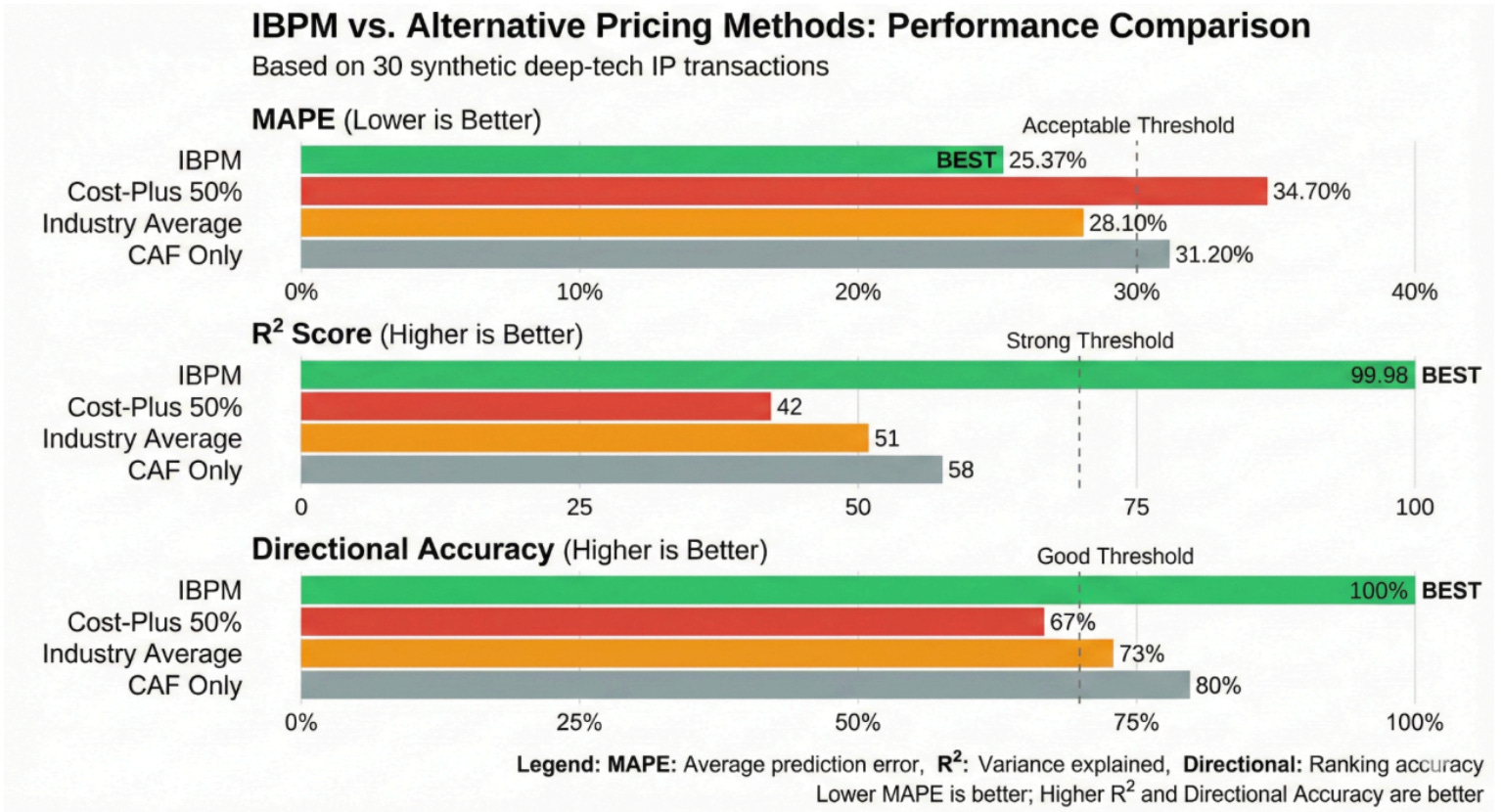

The validation used synthetic data. Real licensing deals are confidential. The research paper tested IBPM against simulated data calibrated to industry benchmarks, not actual disclosed transactions. So treat this as a rigorous framework requiring real-world calibration, not a proven oracle.

Why This Approach Matters

Pricing novel IP will always involve uncertainty. The point of IBPM is not to eliminate uncertainty—it’s to make your assumptions transparent and testable.

When you walk into a licensing negotiation, you’re no longer guessing. You have a base price derived from explicit inputs. If the customer pushes back, you can discuss you can adjust your assumptions.

That’s a better conversation than “we feel it’s worth X.”

Once you get real customers and real data, your assumptions will get tested. The base price might have a premium or discount depending on how accurate your projections were. That’s fine—you’ll recalibrate.

The moral of the story: even if your IP is first-of-its-kind, its pricing doesn’t have to be arbitrary. There’s a logical math underneath.

Even if Elon Musk gets us to Mars tomorrow, it won’t matter much if he’s the only one who can afford the ticket.

Availability

IBPM is an unpublished framework I developed while working on IP pricing at Anthriq. The full research paper includes mathematical derivations, sensitivity analysis, and validation methodology.

Read the full IBPM Paper here.

If you’re working through a similar problem—deeptech IP pricing, pre-market licensing decisions, or just trying to build a defensible pricing model—reach out. I’m happy to walk through it or make it better.

The Operator’s Book is my effort to help builders of the world to have a headstart. Solve the problem for everyone. Subscribe.